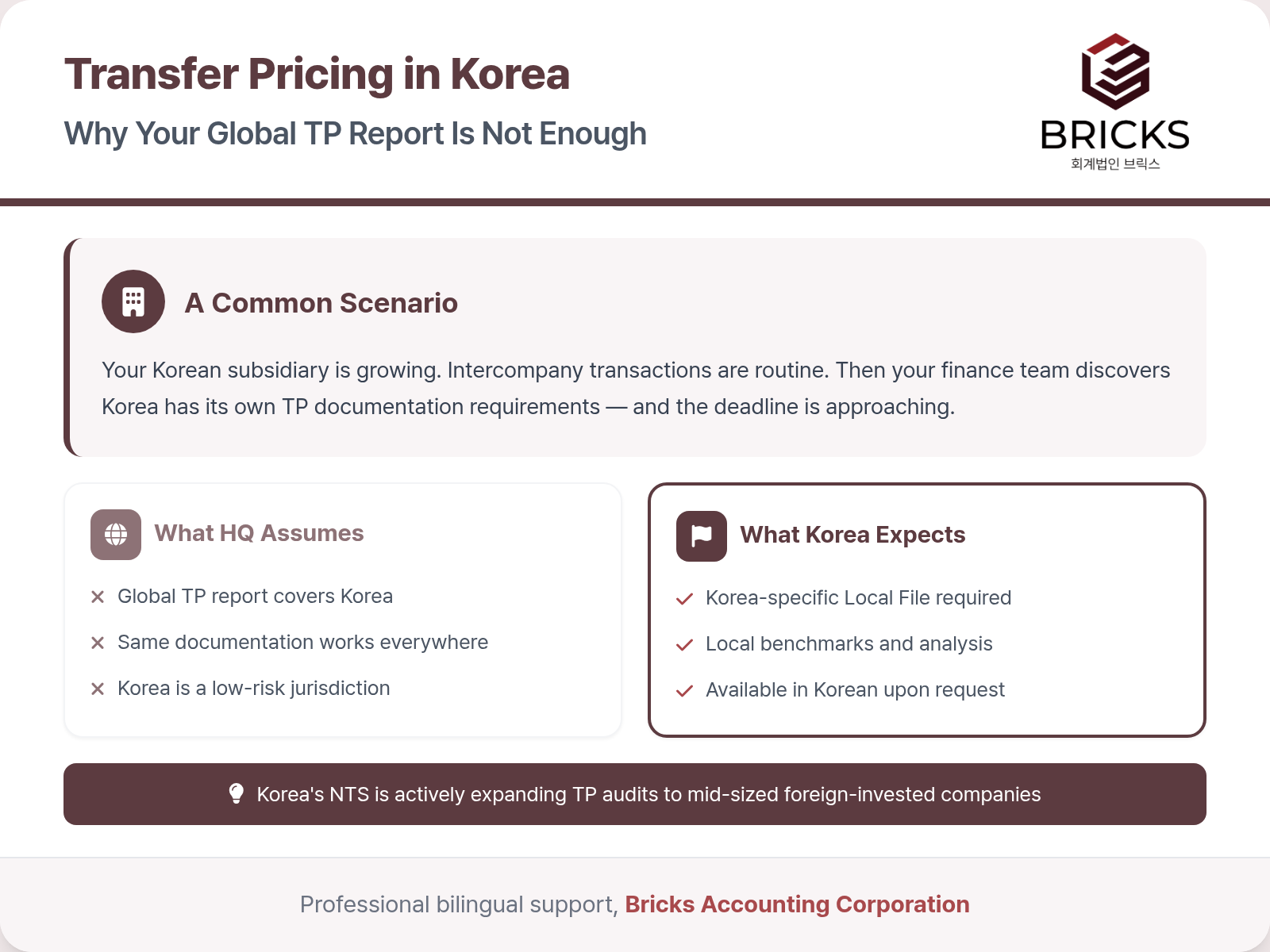

Your Korean subsidiary has been operating smoothly. Sales are growing, and intercompany transactions with headquarters have become part of normal business. Then, during year-end tax preparation, your finance team hears for the first time that Korea may require transfer pricing documentation.

This is a situation we see regularly at Bricks. A foreign headquarters that has managed global compliance for years suddenly discovers that Korea has its own specific requirements, and the deadlines are closer than expected.

This guide is for the person at headquarters who just learned about this obligation. We will explain what Korea requires, what you need to prepare, and what happens if you do not address it in time.

Bricks Accounting Corporation provides bilingual (Korean-English) transfer pricing documentation support for foreign-invested companies operating in Korea. We work directly with your headquarters to ensure your Korean operations meet all local compliance requirements.

The Moment It Becomes Real

Most headquarters assume that their existing global transfer pricing policy covers every jurisdiction, including Korea. In many cases, the group has a global TP report prepared by a Big 4 firm, and the assumption is that this document satisfies local requirements everywhere.

Korea does not work that way. Korean tax authorities expect documentation that specifically addresses the Korean entity’s transactions, uses locally relevant benchmarks, and is available in Korean when requested during an audit. A global report that treats Korea as one line item among dozens of countries will not meet these expectations.

This is not a theoretical risk. Korea’s National Tax Service has been expanding its transfer pricing audits beyond the largest multinationals. Mid-sized foreign-invested companies are now regular targets, and enforcement has been intensifying in recent years.

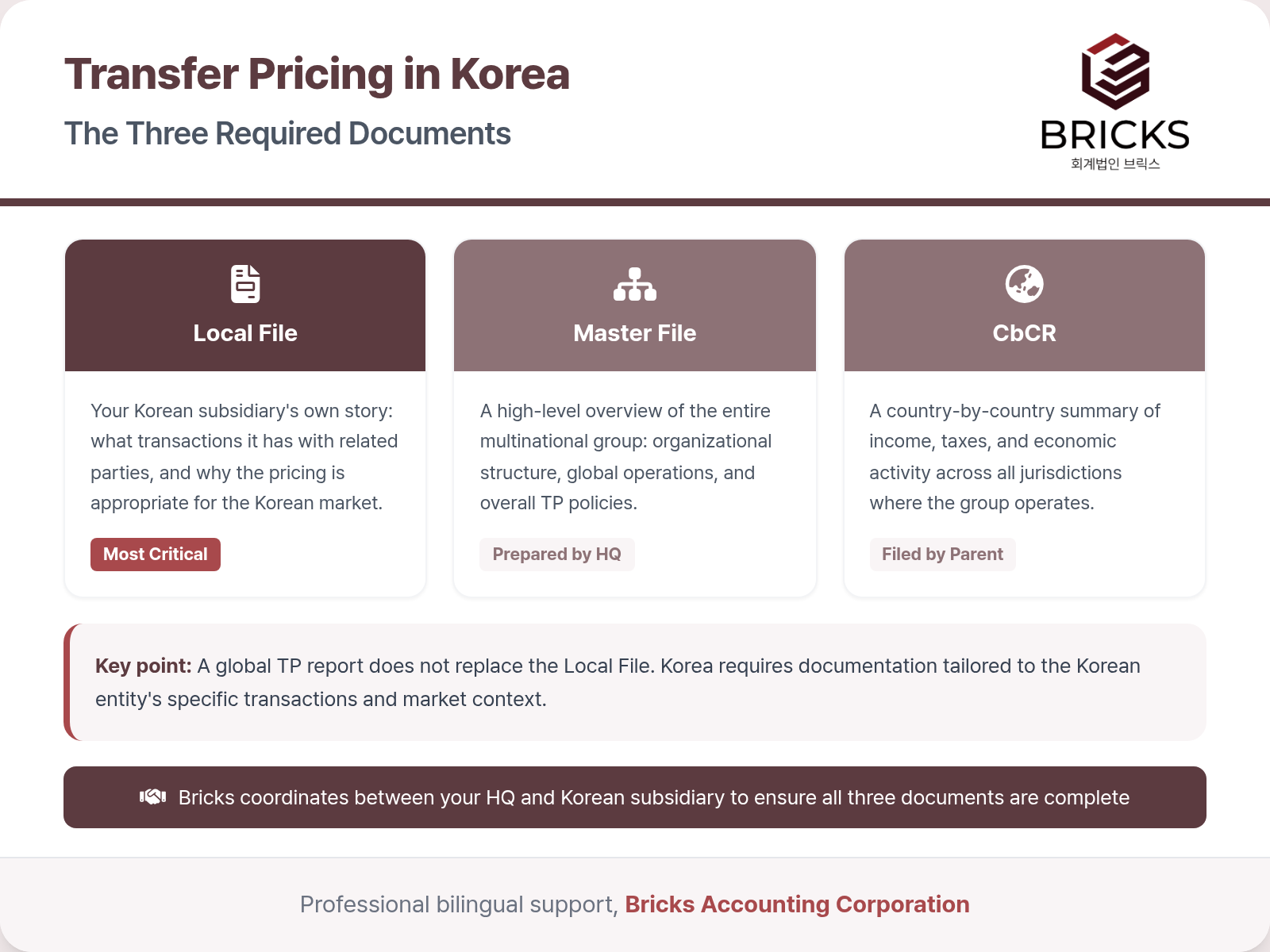

What Korea Requires: Three Documents

Korea follows an internationally recognized three-tier documentation framework. If your group already prepares transfer pricing documentation at the global level, you will recognize the structure. The key difference is that Korea has specific local requirements for each document.

Local File is the most important document from Korea’s perspective. It describes your Korean subsidiary’s intercompany transactions, explains why the pricing is appropriate, and provides supporting analysis using locally relevant data. Think of it as the Korean entity telling its own story to Korean tax authorities.

Master File provides a high-level overview of the entire multinational group, including its organizational structure, global business operations, and overall transfer pricing policies. This is typically prepared at headquarters, but the Korean subsidiary must ensure it is available for Korean tax authorities upon request.

Country-by-Country Report (CbCR) is a summary of how the group allocates income, taxes, and economic activity across all countries where it operates. The filing obligation usually sits with the ultimate parent entity, though Korean subsidiaries may have a secondary filing obligation in certain circumstances.

The critical point for headquarters is this: having a global TP report does not automatically satisfy Korea’s Local File requirement. The Local File must be tailored to the Korean entity’s specific situation.

What Happens If You Miss It

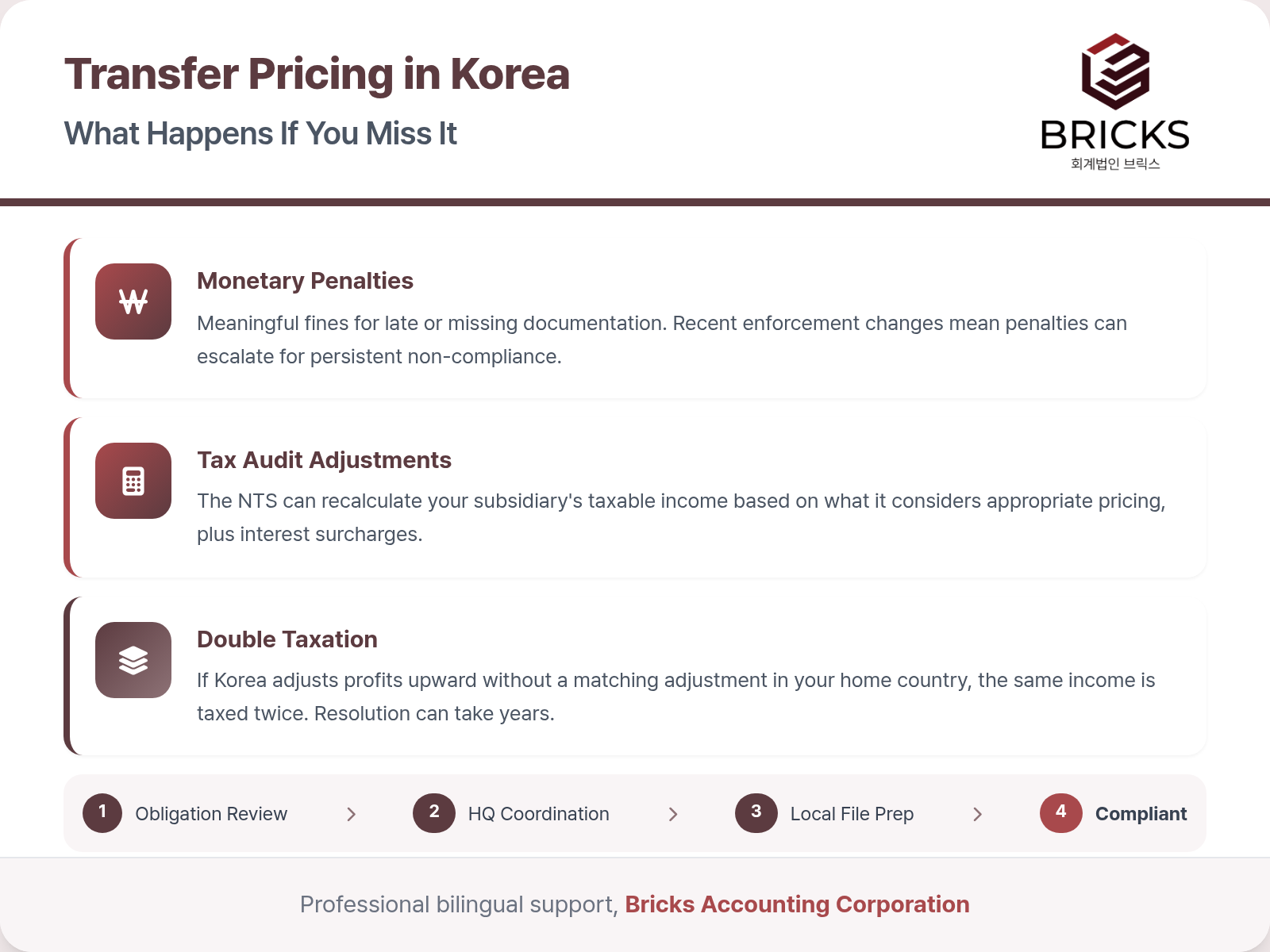

Companies that overlook Korea’s TP documentation requirements face three categories of risk.

Penalties. Korea imposes monetary penalties for late or missing documentation. The amounts are meaningful enough to get attention, and Korea has recently introduced enforcement provisions that can escalate the penalties for persistent non-compliance.

Tax audit adjustments. If Korea’s National Tax Service determines that your intercompany prices do not reflect what independent parties would agree to, it will recalculate the Korean subsidiary’s taxable income accordingly. The resulting additional tax, combined with interest-equivalent surcharges, can be substantial.

Double taxation. This is the risk that concerns headquarters the most. If Korea adjusts the Korean subsidiary’s profits upward, and your home country does not provide a corresponding downward adjustment, the same income is taxed in both jurisdictions. Resolving this through government-to-government procedures can take years, and the outcome is never guaranteed.

None of these outcomes are inevitable. They are the consequences of not having proper documentation in place before they become an issue.

How Bricks Helps You Get It Right

We understand that for many headquarters, Korean TP documentation feels like one more compliance task in a long list. The challenge is compounded by the language barrier, unfamiliar regulatory requirements, and the difficulty of coordinating between the Korean finance team and global TP leadership.

This is exactly the situation Bricks was built to handle. Our approach follows a structured process.

Obligation review. We start by assessing whether your Korean subsidiary has a TP documentation obligation, and if so, which documents are required and when they are due. Many companies are relieved to find that the scope is clearer than they feared.

Data coordination with headquarters. We work directly with your global TP team or headquarters finance team to gather the information needed for the Master File and to understand the group’s intercompany pricing policies. All communication is in English.

Local File preparation. Our CPAs prepare the Local File in accordance with Korean regulatory requirements and National Tax Service expectations. We use locally relevant benchmarks and ensure the analysis reflects the Korean market context.

Ongoing support. Transfer pricing is not a one-time exercise. We provide year-over-year updates and help your team stay ahead of regulatory changes, so you are never caught off guard.

We speak the language of your headquarters and the National Tax Service simultaneously. That is the bridge most foreign-invested companies need but struggle to find.

Next Steps

Not sure whether your Korean subsidiary has a filing obligation? Bricks can review your situation and explain what needs to happen, step by step.

The process is straightforward: we confirm your obligations, help coordinate with your headquarters, and prepare the documentation so your Korean operations remain fully compliant.

Whether you are in Seoul or at your global headquarters, you can reach us in English anytime. Contact Bricks Insight for a consultation, and we will respond promptly.

Reference date: 4월 2026 (based on regulations as of this date)

Bricks Insight | FSC-Registered Accounting Firm (License No. 394)

This content was written and reviewed by Korean Certified Public Accountants of Bricks Insight, a Korean accounting corporation registered with the Financial Services Commission (License No. 394). It is provided for general informational purposes only and does not substitute professional tax, accounting, or legal advice for any specific situation. For matters concerning your individual circumstances, please consult a qualified professional. The information reflects the laws and precedents applicable at the time of writing and may change due to subsequent amendments.