If your company runs a subsidiary in Korea, you have probably experienced this. Quarter-end arrives, and the Korean office sends over financial statements you cannot read. The numbers are in Korean. The format looks unfamiliar. And your global finance team has no idea how to plug them into the consolidation.

You are not alone. This is one of the most common frustrations for foreign companies operating in Korea. The good news is that it does not have to be this way.

BRICS Accounting Corporation helps foreign companies in Korea get clear, accurate English financial reports — prepared right here in Korea by CPAs who speak both languages and understand both Korean accounting practices and global reporting requirements.

The Korean Reporting Challenge

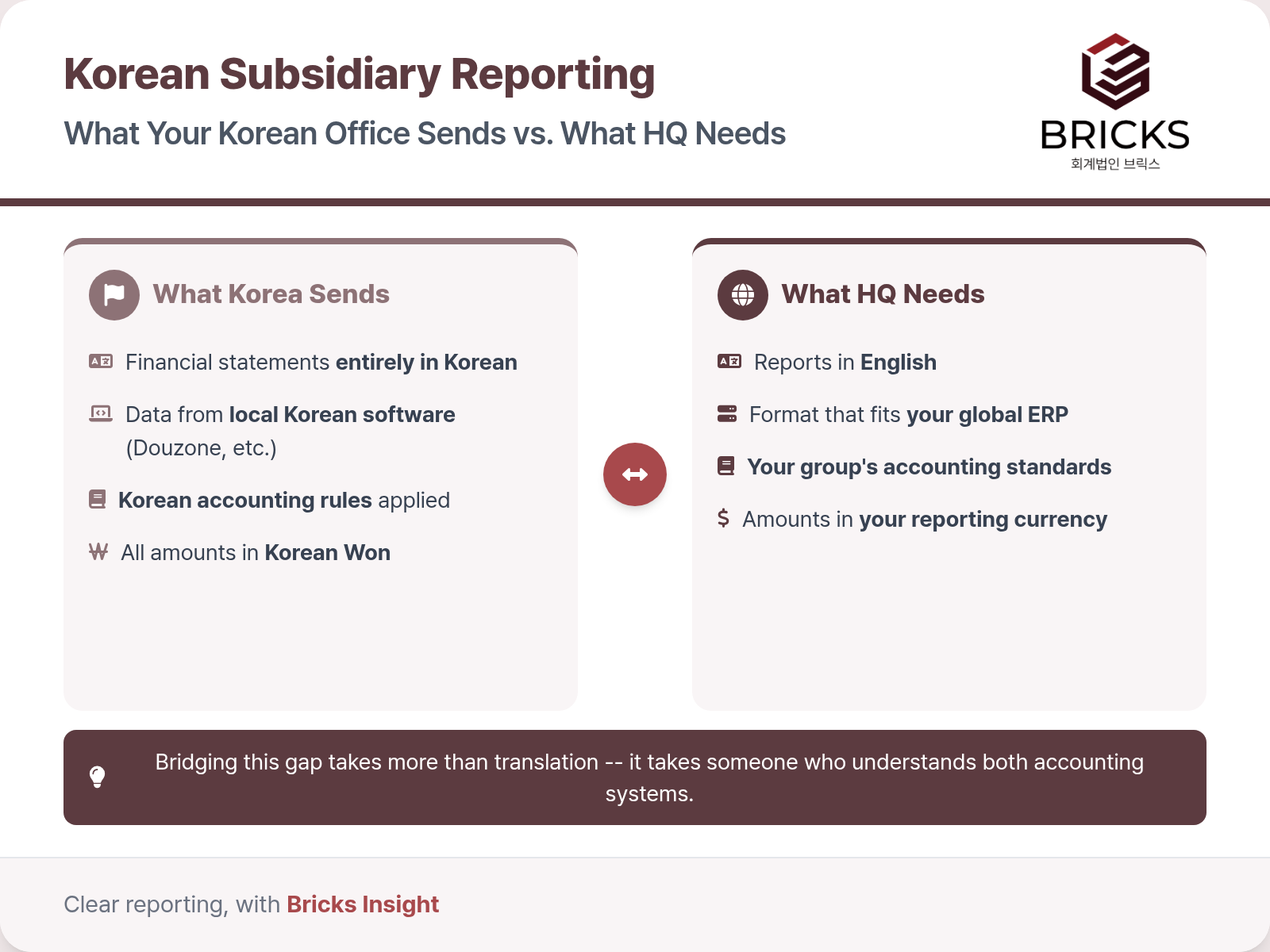

Here is what typically happens. Your Korean entity keeps its books on local accounting software like Douzone. Everything is in Korean — the chart of accounts, the ledgers, the tax filings. This is completely normal. Korean regulations require it.

But your headquarters needs reports in English. Under your group’s accounting standards. In a format that fits your global ERP system. And ideally, delivered before the consolidation deadline.

The gap between these two worlds is where the problems start. It is not anyone’s fault. Korea simply has its own accounting environment — its own rules, its own software, its own reporting calendar. When you try to force Korean books into a global template without a proper process, things break.

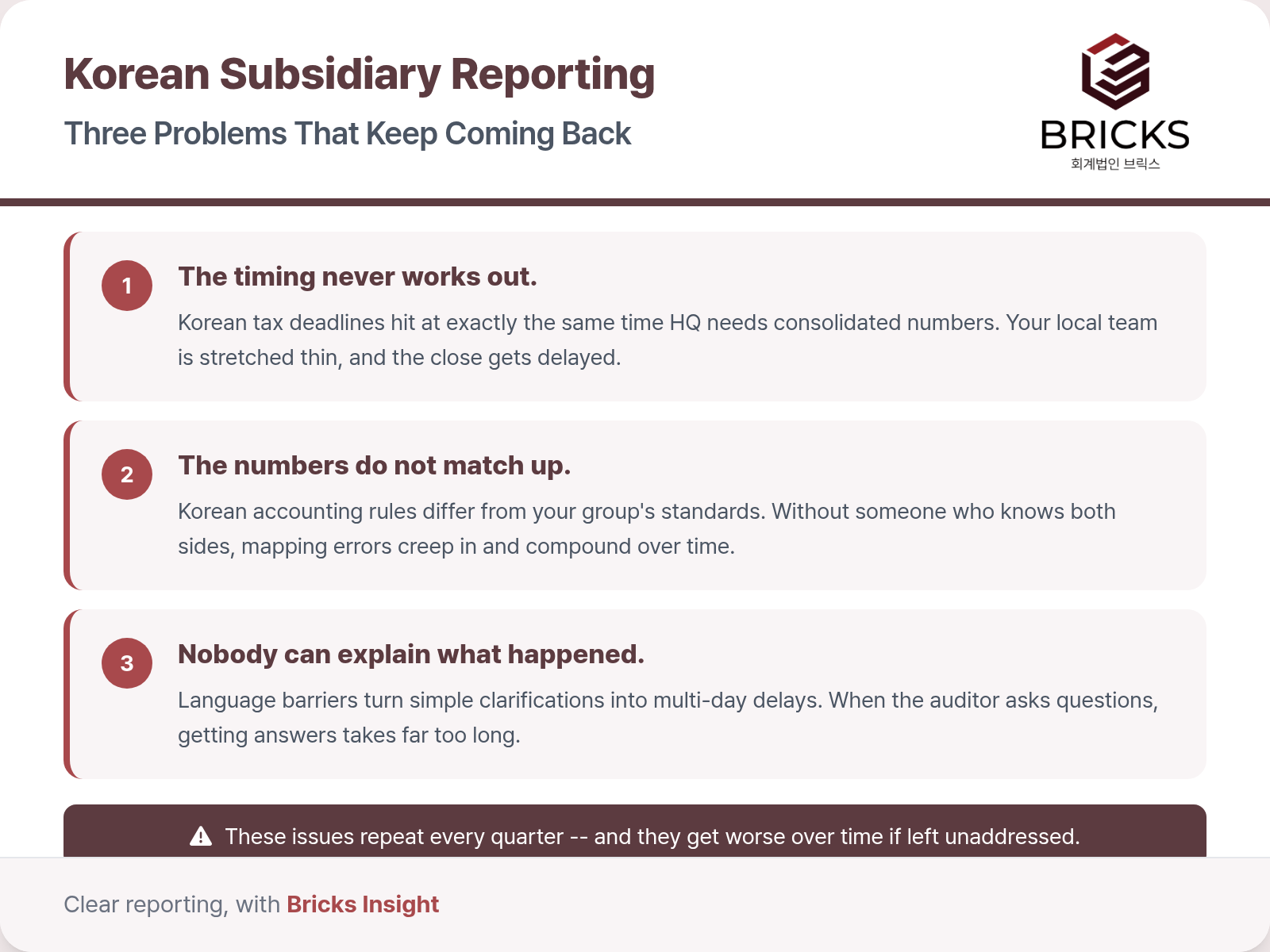

Three Problems That Keep Coming Back

Most foreign companies with Korean subsidiaries run into the same issues, quarter after quarter.

1. Timing conflicts between local deadlines and the group close. Korea has its own strict tax deadlines. VAT returns, corporate income tax, year-end employee tax settlements — these all land at the same time your headquarters needs the consolidated numbers. The local team is stretched thin, and the HQ close gets delayed waiting for Korea.

2. Reconciliation gaps from accounting standard differences. Korean accounting standards have real differences from what your parent company uses. Revenue might be recognized at a different point. Certain liabilities exist in Korea that have no direct equivalent elsewhere. When someone tries to map Korean accounts to your global chart of accounts without deep knowledge of both sides, errors creep in. And they compound over time.

3. Communication barriers between the local team and headquarters. Your Korean accounting team communicates in Korean. Your headquarters finance team communicates in English. When a question comes up about a specific entry, a simple clarification can take days to resolve. If the person who prepared the books cannot explain the reasoning directly to your controller or auditor, the process stalls.

A Structured Approach: Bridging the Two Systems

The solution is straightforward in concept. You need someone who can sit between your Korean books and your headquarters’ requirements — someone who understands both sides deeply enough to translate not just the language, but the accounting logic.

In practice, this means four things.

First, build a proper account mapping. Every Korean account needs a clear link to the corresponding account in your parent company’s chart of accounts. This is not a translation exercise. It requires accounting judgment about how to classify things that do not have a one-to-one match.

Second, extract and convert the trial balance each period. Pull the data from the Korean system, apply the mapping, and convert from Korean Won to your reporting currency using the correct exchange rates.

Third, make the necessary adjustments. Korean accounting rules differ from international standards in specific areas. Certain items need adjusting entries to align with what your parent company expects. The key is to identify these differences upfront and document each adjustment clearly, so your auditor can review them without guesswork.

Fourth, deliver a complete English reporting package. Balance sheet, income statement, cash flow statement, and notes — formatted the way your headquarters needs them.

Once this process is set up properly, it runs smoothly each quarter. The first time takes effort. After that, it becomes routine.

Why This Is Hard to Do In-House

Companies sometimes try to handle this internally. The local Korean accountant prepares an English version, or someone at headquarters tries to reconcile the numbers remotely.

It rarely works well. The Korean accountant knows Korean tax law inside out but may not be familiar with your group’s accounting standards — or comfortable communicating technical details in English. The headquarters staff member knows the group’s requirements but has no visibility into why the Korean books look the way they do.

What you need is a professional who works fluently in both directions. Someone who understands Korean accounting, Korean tax rules, and the local software, while also knowing how to apply international standards and communicate the results clearly in English.

This combination is not common. It is a specialized skill set — and the quality of your Korean reporting depends on whether the people doing the work have handled these cross-border situations before.

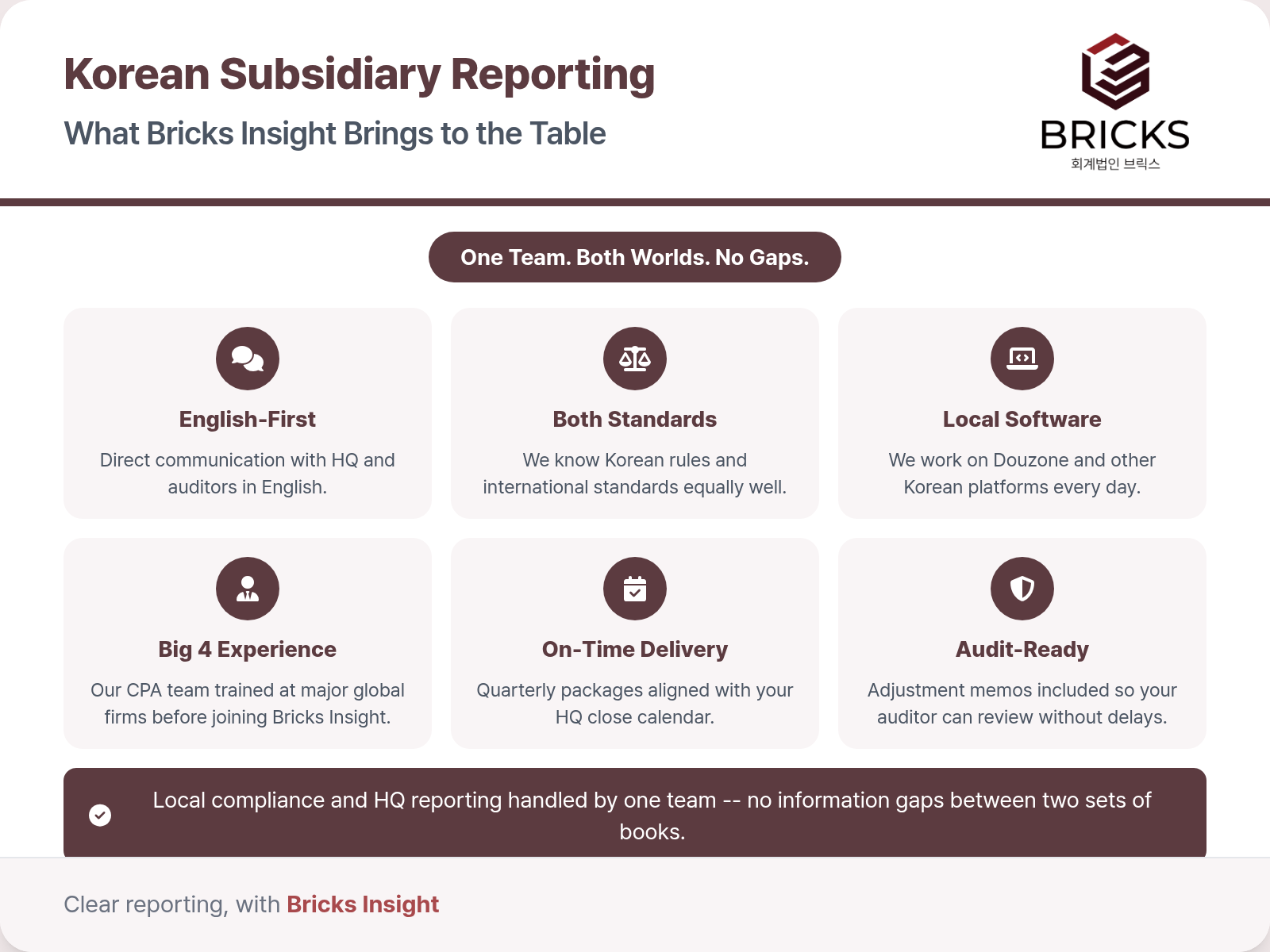

How BRICS Can Help

BRICS Accounting Corporation works with foreign subsidiaries and branches in Korea. We handle both the local Korean compliance and the headquarters reporting as one integrated service.

Our CPA team has Big 4 experience and works with foreign-invested companies every day. We manage the Korean books on local platforms like Douzone, maintain the account mapping to your parent company’s chart of accounts, and prepare the adjusting entries as part of the regular close — not as a last-minute scramble.

What this means for your headquarters: you receive a clean English reporting package on time each quarter. Adjustment memos are included for your auditor. And our team communicates directly with your headquarters finance team in English throughout the process.

Frequently Asked Questions

Does our Korean subsidiary need to use Korean accounting software?

In most cases, yes. Korean tax authorities require real-time electronic invoicing and regulatory filings through locally integrated systems. The software itself is not the problem — the challenge is extracting the data and converting it into a format your headquarters can use. That is where we come in.

How different are Korean accounting standards from IFRS or US GAAP?

There are real differences, particularly around how certain liabilities, revenue, and employee benefits are treated. The specifics depend on your industry and the standards your parent company follows. Rather than trying to learn every detail, the practical approach is to have a specialist identify the differences that affect your consolidated numbers and handle the adjustments for you.

Can we communicate with your team entirely in English?

Yes. Our CPAs conduct all client communications in English — from regular reporting updates to audit support. You do not need a translator or a go-between. Whether you are based in Korea or at your overseas headquarters, you can reach us directly.

Ready to Simplify Your Korean Reporting?

If your Korean subsidiary’s financial reporting has been a source of friction during the quarterly close or annual audit, we would welcome the chance to talk about how we can help. And if you are setting up a new entity in Korea, getting the reporting structure right from the start will save significant time and cost down the road.

Whether you are in Seoul or at your global headquarters, you can reach us in English anytime. Contact Bricks Insight for a consultation, and we will respond promptly.

Reference date: 4월 2026 (based on regulations as of this date)

Bricks Insight | FSC-Registered Accounting Firm (License No. 394)

This content was written and reviewed by Korean Certified Public Accountants of Bricks Insight, a Korean accounting corporation registered with the Financial Services Commission (License No. 394). It is provided for general informational purposes only and does not substitute professional tax, accounting, or legal advice for any specific situation. For matters concerning your individual circumstances, please consult a qualified professional. The information reflects the laws and precedents applicable at the time of writing and may change due to subsequent amendments.